New analysis suggests that the Government’s proposed state pension tax exemption could leave millions of older retirees out, creating what experts warn may be “serious unfairness” and steep financial cliff edges. The scheme, expected to take effect in 2027/28, is projected to benefit only around 5.4% of pensioners, roughly one in 18, according to LCP, a leading pension consultancy.

Why Many Pensioners Could Face Tax

Under the proposal, pensioners who reached state pension age before April 6, 2016, will effectively be excluded, even if their total retirement income matches those who qualify. This is because the exemption applies only to retirees whose sole income is the new basic state pension, with no additions or increments.

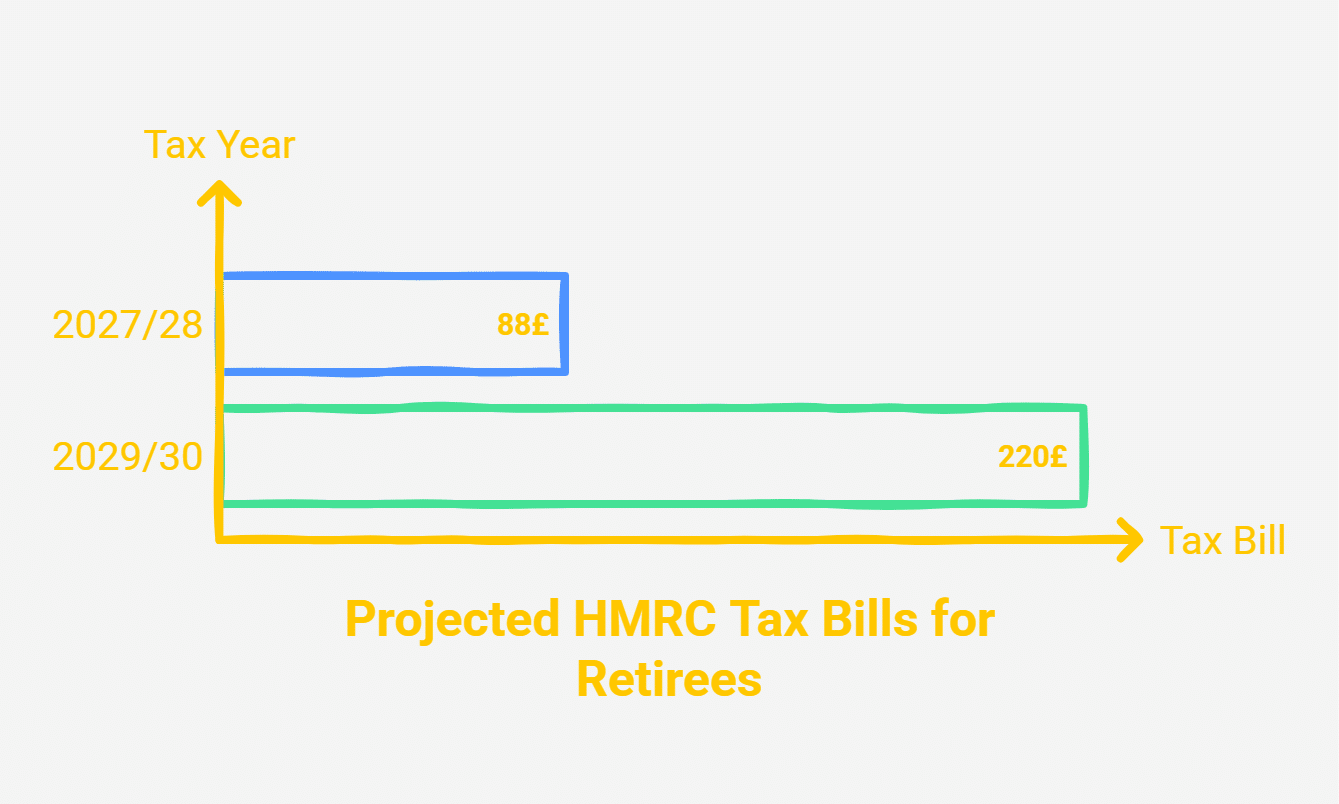

Rising state pension amounts under the triple lock, which increases pensions annually by inflation, average earnings, or 2.5%, are outpacing the frozen personal allowance of £12,570. Analysts predict that many retirees could face HMRC tax bills starting at around £88 in 2027/28, rising to £220 by 2029/30.

Only a Small Fraction Will Benefit

Of the roughly 13.2 million state pension recipients in the UK, LCP estimates that 7.7 million on the old system will automatically miss out. Even among the 5 million on the new state pension, most will be disqualified due to extra income, protected payments, or overseas residency. Only around 700,000 pensioners are expected to benefit from the tax break.

Experts warn this could create inequitable outcomes where two retirees with identical total income are treated differently. A pensioner receiving only the new state pension may qualify, while another with the same total income through the old pension plus SERPS or State Second Pension could still face a tax bill.

Cliff Edges and Small Private Pensions

Even modest additional income can push retirees over the threshold, nullifying the exemption. Workplace pensions, small annuities, savings, or automatic enrolment pots could inadvertently trigger higher tax bills, creating sharp financial cliff edges. Pension specialists say the plan adds complexity and unfairness to a system meant to simplify pension taxation.

Long-Term Costs and Policy Challenges

As the state pension continues rising faster than the frozen personal allowance, the exemption’s cost will grow. By 2029/30, qualifying pensioners could receive more than £200 annually in waived tax, making the scheme expensive and politically challenging to reverse. Experts suggest broader reforms, such as increasing the personal allowance for all pensioners or writing off small tax bills, could address inequities, though these carry fiscal costs.

The policy highlights the challenge of balancing fairness, simplicity, and affordability, leaving millions of pensioners over 75 potentially paying tax despite having no other income.