For generations, owning a home has been closely tied to the American dream and the accumulation of wealth. Today, that aspiration remains widespread, but many prospective buyers are finding themselves priced out of the market as affordability continues to deteriorate.

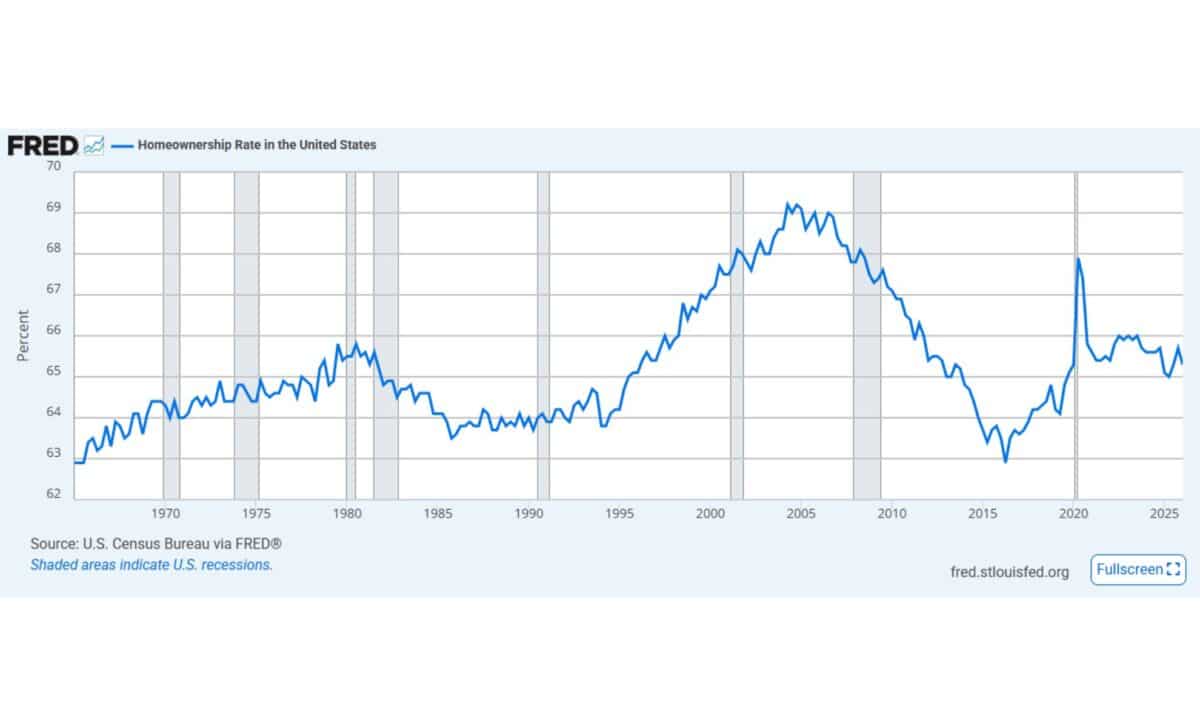

The U.S. housing market has entered what several economists describe as an unprecedented period. According to Newsweek, home prices have climbed by roughly 60 percent since the beginning of the COVID-19 pandemic, while mortgage rates have remained at their highest levels in years. At the same time, the national homeownership rate fell to 65 percent in 2025, its lowest point since 2019, according to U.S. Census data cited by the publication.

Daryl Fairweather, chief economist at Redfin, told Newsweek that the current combination of record home prices and relatively high borrowing costs has made entering the housing market especially difficult for younger Americans who do not already own property.

Homeownership Remains Central to the American Economy and Identity

Economists interviewed by Newsweek said homeownership has long occupied a unique place in American society. Fairweather explained that ideas surrounding property ownership date back to the country’s founding and were influenced by political thinkers such as John Locke, while later policies, including the Homestead Act of 1862, expanded opportunities for settlers to acquire land.

Joel Berner, senior economist at Realtor.com, said policymakers have historically encouraged homeownership as a way to build generational wealth and strengthen the middle class. According to Realtor.com, roughly two-thirds of Americans surveyed in 2025 still identified owning a home as a personal goal.

Fairweather noted that homeowners generally accumulate substantially more wealth than renters and that federal tax policies continue to provide financial advantages for homeownership. She also said that after the housing crash of 2007 and 2008, the belief that expanding homeownership alone could broadly increase prosperity proved unsustainable under lending practices that relied on subprime mortgages and weak regulation.

Brad Case, chief residential economist at Homes.com, told Newsweek that housing affordability began changing when home prices started rising faster than both inflation and household incomes after mortgage rates declined from the elevated levels of the 1970s and early 1980s. He argued that homes increasingly came to be viewed as investments rather than simply places to live, influencing public policy and local resistance to new housing development.

High Borrowing Costs and Limited Supply Have Created a Stalled Market

According to Newsweek, today’s housing market differs from previous cycles because rising mortgage rates have not been accompanied by broad declines in home prices. Fairweather said both buyers and sellers have retreated at the same time, resulting in fewer transactions while prices have remained stubbornly high.

She also said many homeowners who secured mortgage rates near 3 percent during 2020 and 2021 are reluctant to sell because purchasing another home would require financing at current market rates. At the same time, buyers continue to face both elevated prices and higher borrowing costs.

Berner described the current affordability challenge as structural rather than the type of acute market collapse seen in previous downturns. He said efforts to improve affordability are increasingly focused on reducing regulatory barriers to new construction, although those measures are expected to have gradual rather than immediate effects.

Looking ahead, the economists interviewed by Newsweek said affordability could improve over time as wage growth catches up with slower home price increases and housing supply gradually expands in some regions. Fairweather also said the transfer of homes from aging baby boomers to younger generations may improve access in certain markets, although she cautioned that rising insurance costs, aging housing stock, and persistent shortages in high-demand metropolitan areas will continue to present significant challenges.