The income needed to afford a median-priced home has risen sharply since 2020, with new data showing that households now need close to twice the earnings required five years ago, reflecting higher mortgage rates, rising home prices and weaker housing demand conditions across recent years.

Housing Affordability And Income Requirements

The report shows that the income required to afford a median-priced home in the United States has moved from around $66,000 in 2020 to more than $120,000 in 2025. The change is linked to a combination of higher borrowing costs and sustained price growth in both new and existing housing.

Median home prices now sit above $400,000 for both new and existing properties. At the same time, existing home values have increased by about 54 percent since 2020, creating a wider gap between household earnings and purchase prices.

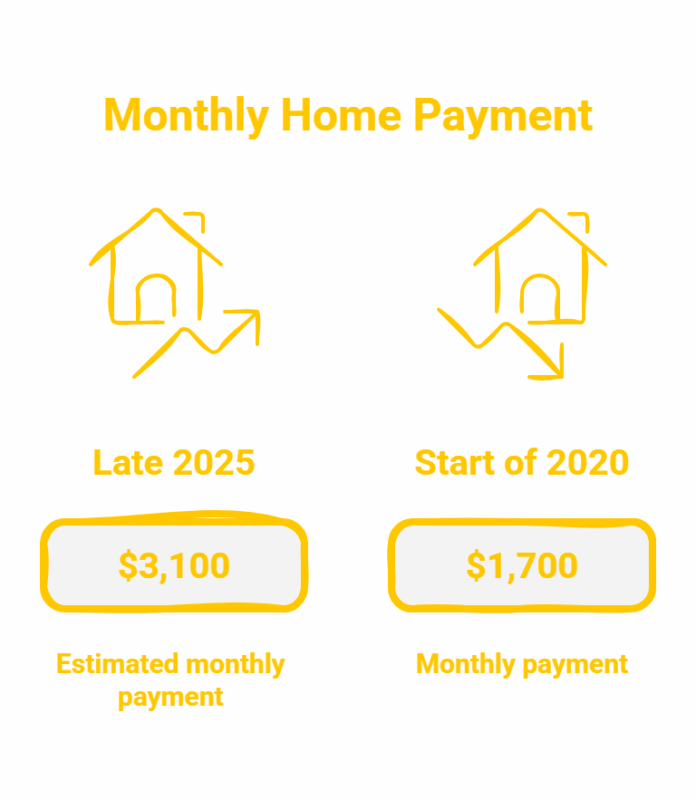

Mortgage rates above six percent have also added pressure to monthly repayments. A median-priced home now carries an estimated monthly payment of around $3,100 in late 2025, compared with roughly $1,700 at the start of 2020.

Home Prices And Mortgage Costs

Higher borrowing costs have reshaped affordability calculations across the housing market. The report notes that the ratio between home prices and income has moved well beyond historical averages. In the 1990s, a common benchmark placed home prices at around three times median income. Current estimates place that ratio closer to five times.

This shift has altered buying capacity for many households, particularly first-time buyers. Rising monthly repayment levels have reduced the number of households able to qualify for standard mortgage products based on typical income thresholds.

Lending conditions remain influenced by interest rate levels, with affordability testing applying stricter pressure on new applications. These conditions have contributed to reduced home purchase activity in several regions.

Labour Market And Housing Demand

Changes in employment trends have also played a part in housing demand. Job growth slowed from around 1.5 million gains in 2024 to approximately 116,000 in 2025, reflecting a weaker labour market environment.

Consumer confidence also declined during 2025 and moved lower in early 2026. The report links this shift partly to geopolitical tensions and economic uncertainty, including the Iran war, which contributed to a further drop in sentiment indicators.

Lower confidence levels tend to reduce household mobility, with fewer people willing to move, purchase homes or form new households. The report notes that graduates and younger workers are particularly affected during periods of weaker hiring activity.

Homeownership And Rental Trends

Homeownership growth has slowed, with the rate of increase in homeowner households cut by around half. This has led to a second consecutive annual decline in homeownership rates. Rental market growth has also moderated. The increase in renter households during the first quarter of 2026 was less than half of the growth recorded a year earlier.

High housing costs combined with limited supply have contributed to weaker demand conditions across both ownership and rental segments. The report points to a housing market shaped by pricing pressures, borrowing conditions and slower income growth relative to property values.

It’s crazy how home prices keep climbing. Do you think it’ll affect wedding budgets too?