Millions of Britons are losing money on their savings because their bank accounts pay less interest than the current rate of inflation. Experts say many households are unknowingly missing out on hundreds of pounds every year by leaving cash in low-paying accounts.

Billions of Pounds Are Sitting in Low-Interest Accounts

New analysis based on CACI data and published by savings app Spring shows that around £612.4 billion is currently held in savings accounts paying 3 per cent interest or less. At the same time, UK inflation is running at 3.3 per cent, meaning many savers are effectively losing purchasing power even if their account balances continue increasing on paper.

The figures cover around 69.4 million savings accounts, with the average balance in accounts earning 3 per cent or less standing at approximately £8,812. For many households, the issue is not a lack of savings but where the money is being held.

Savers Could Be Missing Out on Hundreds of Pounds

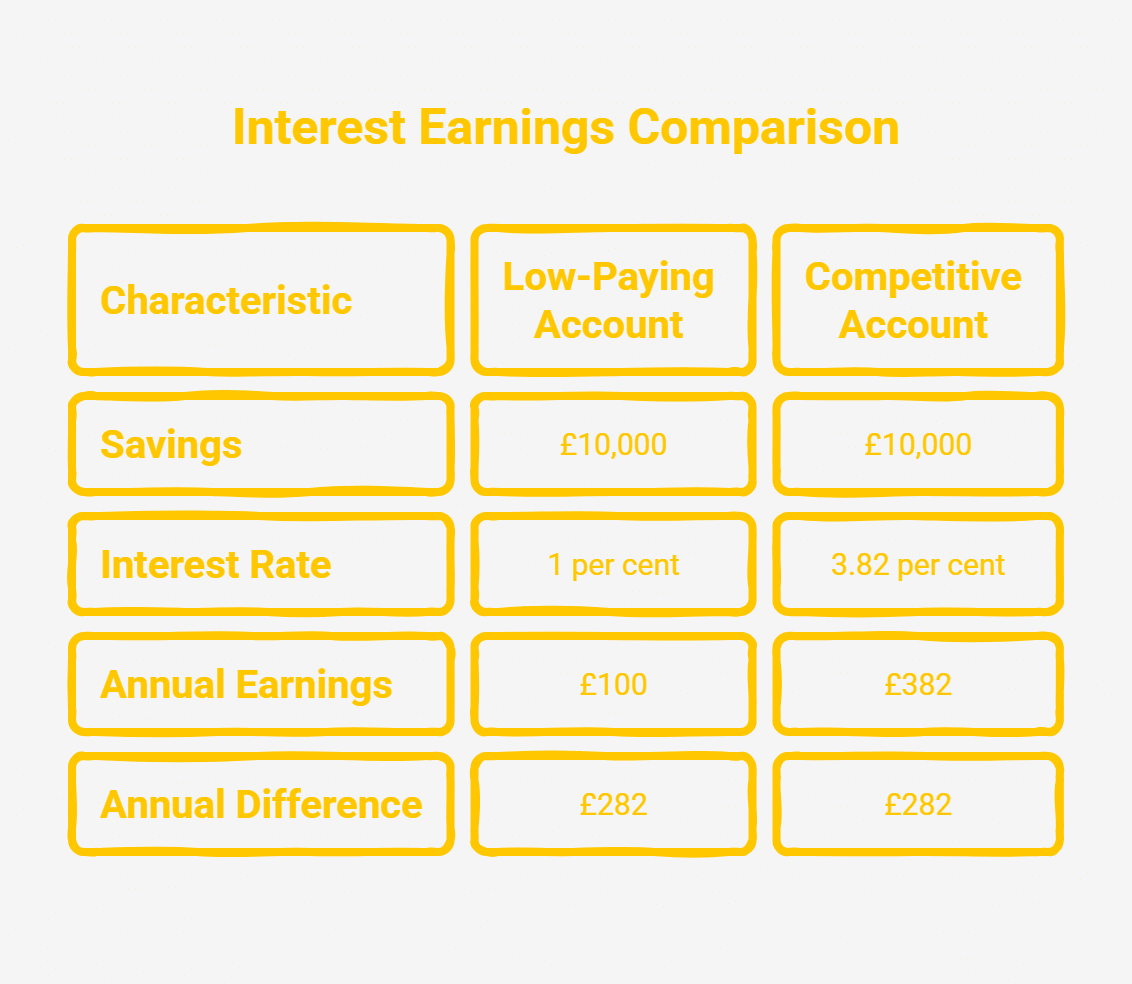

The difference between low-paying accounts and more competitive deals has become substantial. Someone with £10,000 saved in an account paying just 1 per cent interest would earn only £100 over a year. By comparison, a competitive easy-access account paying around 3.82 per cent could generate approximately £382, creating a gap of more than £280 annually.

For savers holding larger balances, the difference grows rapidly over time. According to the data, around £538.9 billion is sitting in accounts containing more than £10,000, while roughly £185 billion is held in accounts with balances exceeding £100,000, all earning below 3 per cent interest.

Many traditional high street banks continue offering rates between 1 per cent and 2 per cent, substantially lower than some online competitors.

Inflation Is Quietly Reducing Spending Power

Financial analysts warn that inflation can erode savings much faster than many consumers realize. Even if account balances rise slightly each year, prices may still increase at a faster pace, reducing what the money can actually buy in the future.

Hargreaves Lansdown analyst Clare Stinton warned to Independent that the long-term effect of inflation on cash savings is frequently underestimated. She noted that an item costing £10 in 2016 would now cost around £14, illustrating how inflation steadily reduces purchasing power over time.

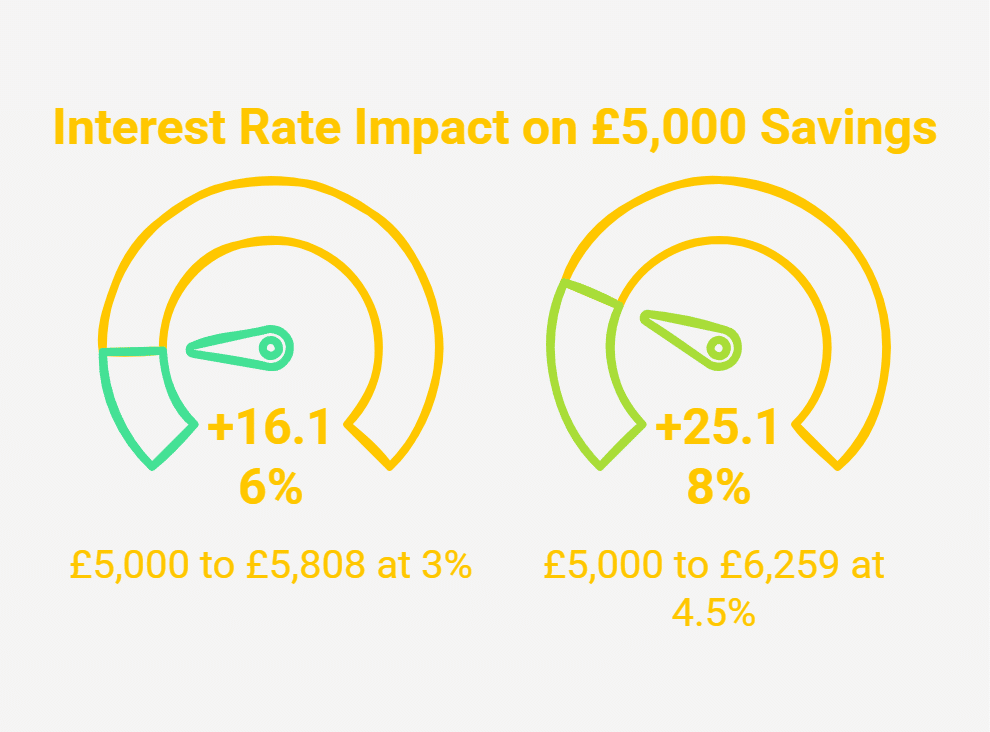

Calculations from Hargreaves Lansdown also show how interest rates dramatically affect long-term savings growth. A £5,000 balance earning 3 per cent interest would grow to approximately £5,808 after five years, compared with roughly £6,259 at a 4.5 per cent rate. Over 15 years, the difference becomes even larger.

Many Savers Stay With Banks Out of Habit

Experts say one of the biggest reasons people lose money on savings is simple inertia. Research from Spring found that around 31 per cent of savers keep money with their existing bank out of habit, while others worry about losing quick access to their funds if they switch accounts.

Financial experts describe this situation as a “loyalty penalty,” where long-term customers often receive weaker rates than new customers or those actively comparing deals. Moneyfacts also reported that some older easy-access savings accounts still pay less than 1 per cent interest.

According to analysts, easy-access accounts paying more than 4 per cent remain available in the current market, while some fixed-rate products and ISAs are offering rates closer to 4.5 per cent. For many households, simply reviewing an old savings account could lead to noticeably better returns over the coming years.