Deciding whether to buy or rent a home remains a hypothetical discussion for most people. Many cannot afford to buy a property or even to leave the family home to find a place to rent. So, let’s analyse the financial implications of owning versus renting a home in the UK.

By looking at average house prices, rents, mortgage rates and repair costs, the aim is to provide a broad comparison of these two housing options over the last 25 years.

Historical Context and Initial Costs

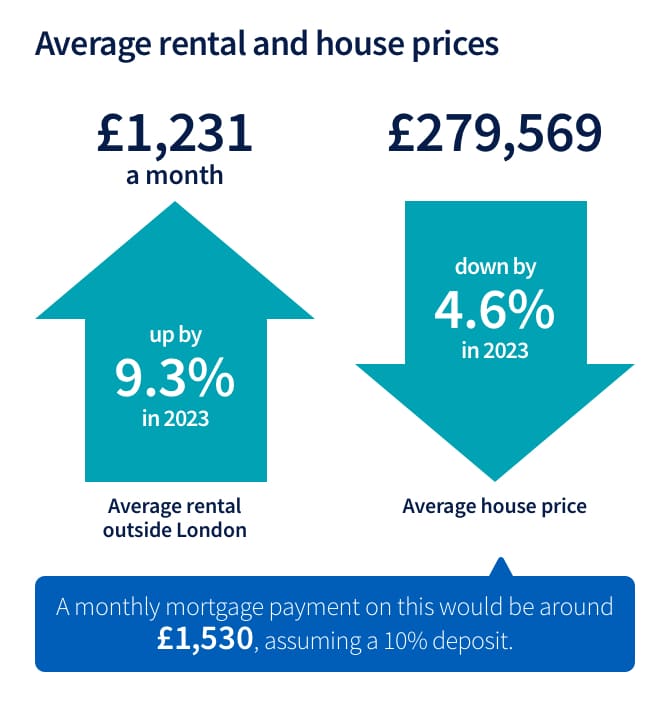

In 1999, the average value of a property was £81,628, and the typical monthly rent for such a property was £450. At that time, the interest rate was 6%.

For tenants, the average annual rent increase was between 2% and 3%. Therefore, today’s monthly rent for the same property would be around £1,200. Over 25 years, the total expenditure on rent would be £172,964, with no financial return.

On the other hand, home buyers face additional costs, particularly for repairs and maintenance. Assuming a full mortgage at 6% interest in 1999, the initial monthly mortgage payment would have been £408.

Over 25 years, with a weighted average interest rate of 4.29%, the average monthly payment would be £444, giving a total of £133,212.

In addition, repairs are estimated at an annual average of 1% of the value of the house, equating to £20,407 over 25 years.

Financial Outcomes of Buying vs Renting

To sum up, the total cost of owning a home, including mortgage payments and repairs, is £153,619. This represents a saving of £19,345 compared with renting. In addition, the increase in the value of the property has a significant impact on the overall financial benefit.

With the average price of a home today at £285,000, the initial investment of £81,628 translates into a gain of £203,372. Therefore, the net benefit of buying versus renting over 25 years is £222,717.

Assuming the average buyer buys at 32 and pays off their mortgage at 57, they will live mortgage-free until the average life expectancy of 81, or 24 years.

The rent saved over those 24 years, assuming an annual increase of 2%, would be £257,280. The overall financial advantage of buying a home over renting is therefore £479,997.

Market Cycles and Strategic Purchasing

Historically, market trends reveal the main drivers of property booms and busts, including interest rates, economic conditions, government policies, financial deregulation, world events and investor behaviour.

- 1920s: Post-war boom, followed by the Great Depression.

- Post-WWII: Housing shortages led to a boom; market cooled in the late 1950s to early 1960s.

- 1970s: Economic growth and relaxed lending fuelled a boom; the 1973 oil crisis triggered high inflation and a crash.

- 1980s: Financial deregulation led to another boom; the 1990s recession caused by high interest rates and a global slowdown resulted in a crash.

- Late 1990s to 2008: Low interest rates and economic growth led to a surge, halted by the financial crisis.

- 2010 onwards: Continued low interest rates and a surge during the COVID-19 pandemic drove the latest market push.

From a strategic point of view, it is essential to recognise downturns and avoid buying during periods of market euphoria in order to maximise financial gains.