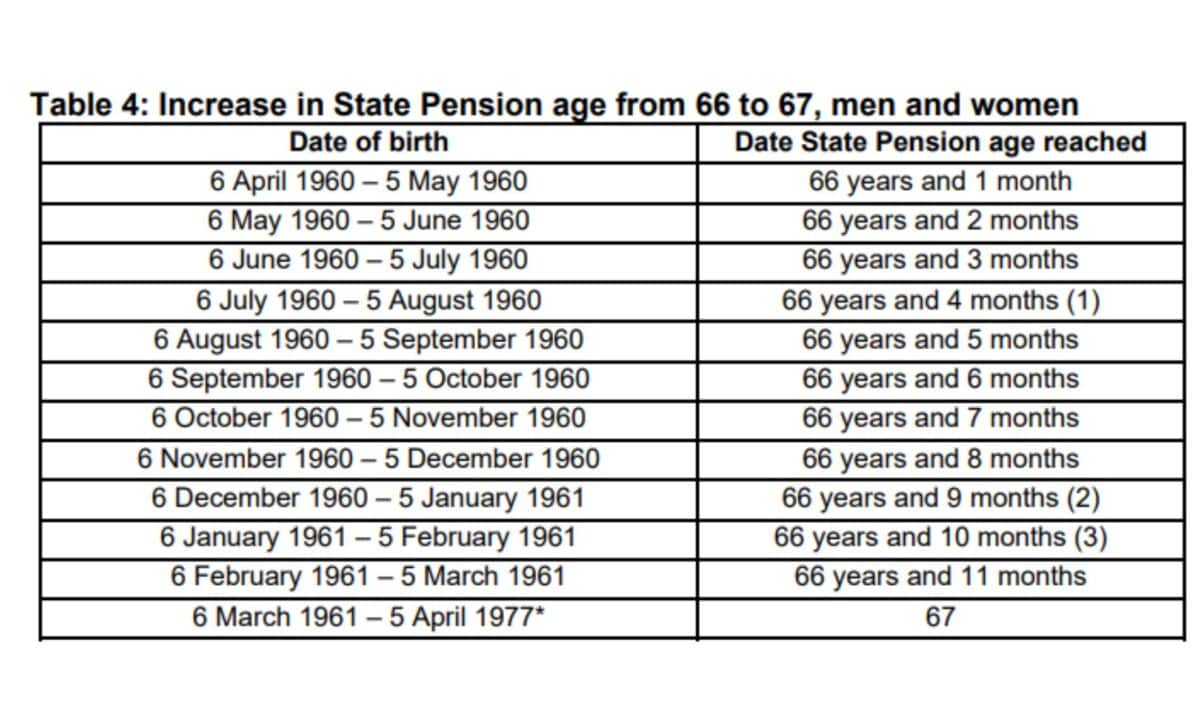

People born between 6 July 1960 and 5 August 1960 will become the latest group affected by the phased increase in the UK’s State Pension age. From 6 July, they will qualify for their State Pension at 66 years and four months rather than at age 66.

The change forms part of the timetable set out under the Pensions Act 2014, which is gradually increasing the State Pension age from 66 to 67 between 2026 and 2028. According to the Department for Work and Pensions (DWP), the increase is being introduced in monthly stages based on an individual’s date of birth.

The revised timetable applies equally to men and women and affects those born between 6 April 1960 and 5 April 1977. Each monthly birth cohort faces an additional month before becoming eligible to claim the State Pension until the qualifying age reaches 67.

For those with birthdays between 6 July and 5 August 1960, the qualifying age is now 66 years and four months. The adjustment follows earlier phases introduced for people born from April 1960 onwards.

July Marks the Next Step in the Phased Timetable

According to the DWP, the current phase begins on 6 July and covers everyone born from 6 July 1960 to 5 August 1960. Individuals in this group will reach State Pension age at exactly 66 years and four months.

The department has published a full schedule covering the transition. People born between 6 April and 5 May 1960 become eligible at 66 years and one month, with each subsequent monthly birth group waiting an additional month. Those born between 6 March 1961 and 5 April 1977 will qualify at age 67.

The official timetable also notes how eligibility is calculated for people born on dates that do not occur every month. For example, a person born on 31 July 1960 is treated as reaching the age of 66 years and four months on 30 November 2026.

According to the Government’s published guidance, a State Pension age calculator is available through GOV.UK, allowing people to check the age at which they become eligible under current legislation.

Research Highlights the Financial Impact of Later Eligibility

Research cited by the Institute for Fiscal Studies (IFS) suggests that previous increases in the State Pension age have influenced employment patterns among older people. According to the IFS, employment rates for the affected age groups rose by around 10 percentage points following earlier increases in the pension age.

The institute said this increase was driven by people remaining in their existing jobs for longer rather than moving into new employment or returning to work after leaving the labour market. It also found that only a minority of those affected extended their working lives, meaning the additional earnings only partly compensated for the delay in receiving the State Pension.

According to the IFS, average household incomes were lower among those required to wait longer before claiming their pension. Its research also found that when the State Pension age increased from 65 to 66, the income poverty rate among affected 65-year-olds rose from 10% to 24%, with the impact concentrated among people who were not in paid work.

Sarah Pennells, consumer finance specialist at Royal London, said understanding an individual’s State Pension age is important because it helps people plan their retirement income. She said knowing the date of eligibility makes it easier to estimate how much needs to be saved in workplace or personal pensions, and when those savings may need to be accessed.