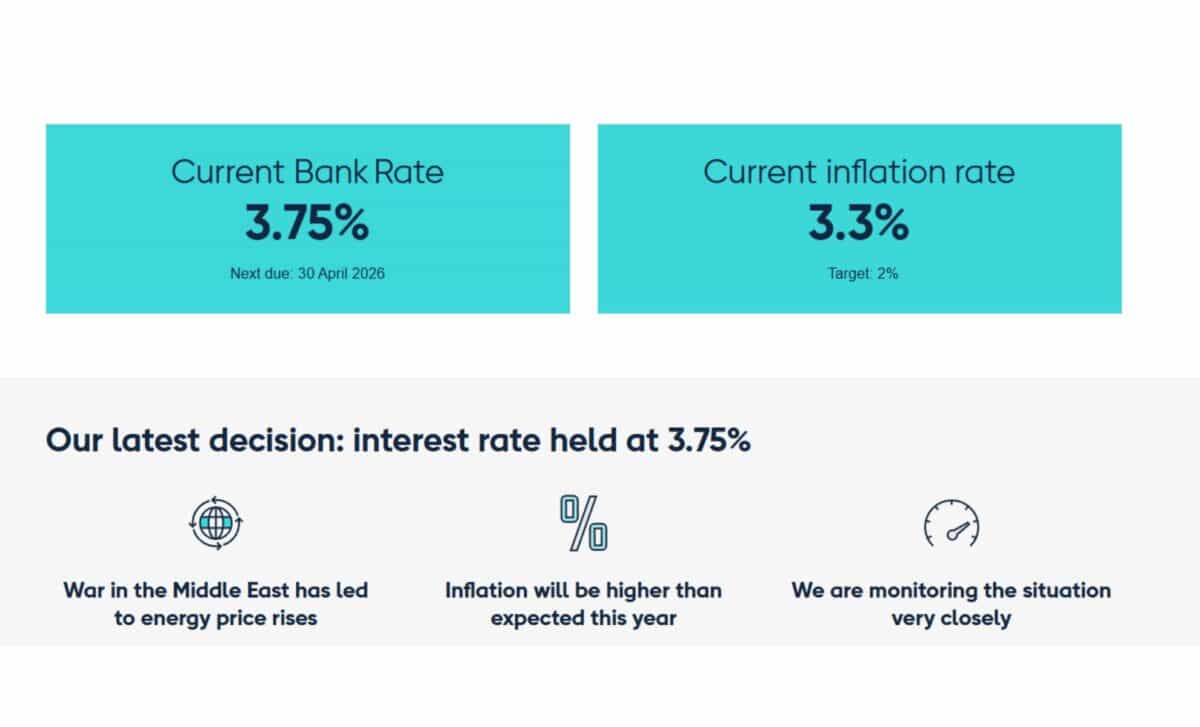

The Bank of England is widely expected to keep its base interest rate unchanged at 3.75% this week, maintaining a cautious stance as uncertainty linked to the Iran conflict continues to weigh on the economic outlook. Investors, though, are increasingly positioning for rate increases later in the year.

This moment reflects a delicate phase for policymakers. Inflation pressures are showing signs of persistence, while economic indicators point to a potential slowdown. The Monetary Policy Committee (MPC) must navigate these competing risks without clear visibility on how external shocks will unfold.

Inflation Concerns Persist as Policymakers Weigh Timing

The central challenge facing the Bank lies in the risk that inflation could rise again, driven in part by higher energy costs and increased input prices for businesses. According to the International Monetary Fund, UK inflation could reach around 4% this year, keeping it among the highest in the G7.

Recent data has reinforced these concerns. Firms have reported rising costs and have increased their expectations for price growth over the next 12 months, according to Reuters. This has raised the possibility that inflation could become more embedded in wage demands and pricing behaviour.

Within the MPC, there are signs of diverging views. While a Reuters poll indicates an 8–1 vote in favour of holding rates steady, some analysts suggest that up to three members could support an immediate increase to 4.0%. The Bank’s chief economist, Huw Pill, has questioned the effectiveness of a “wait and see” approach, noting in mid-April that delaying action risks missing the opportunity to contain inflation pressures.

Financial markets appear more convinced that tightening will resume. Investors have fully priced in a 0.25 percentage point increase in July and another in September, with a small chance of a third rise before the end of the year, according to market pricing data reported by Reuters.

Growth Fears Complicate the Outlook for Interest Rates

At the same time, concerns about economic weakness are becoming more pronounced. Indicators point to softer hiring trends and declining confidence among both consumers and businesses. This raises the risk that premature tightening could deepen a slowdown.

Britain’s exposure to energy price fluctuations adds another layer of vulnerability. The economy is seen as particularly sensitive to rising gas prices, which have been influenced by the ongoing conflict involving Iran. According to Reuters, this exposure could amplify both inflationary pressures and the drag on growth.

Some MPC members are expected to emphasise that the full impact of the energy shock has yet to be felt. They argue that raising rates too soon could compound existing pressures on households and businesses already dealing with higher costs.

The Bank is therefore likely to maintain its existing guidance that it stands “ready to act” if necessary, without signalling immediate changes. According to economist Thomas Pugh of RSM, any hawkish tone in the Bank’s communication should not be interpreted as a firm indication of imminent rate increases, as the economic data could weaken further in the coming months.

Fresh forecasts due alongside the decision are expected to show higher inflation alongside weaker growth extending into 2026 and 2027. For households, a pause in rates may offer short-term stability, though the broader outlook remains uncertain as markets continue to anticipate further tightening.