The 2024 rise in the amount of households wanting to fix their mortgage rate for just a couple of years is an indication of the fact that homeowners are hopeful of falling rates and hence better offers in 2026.

Most UK households have fixed mortgages where interest rate and repayments are locked for set periods, but until recently two-year fixes were less popular than five year ones.

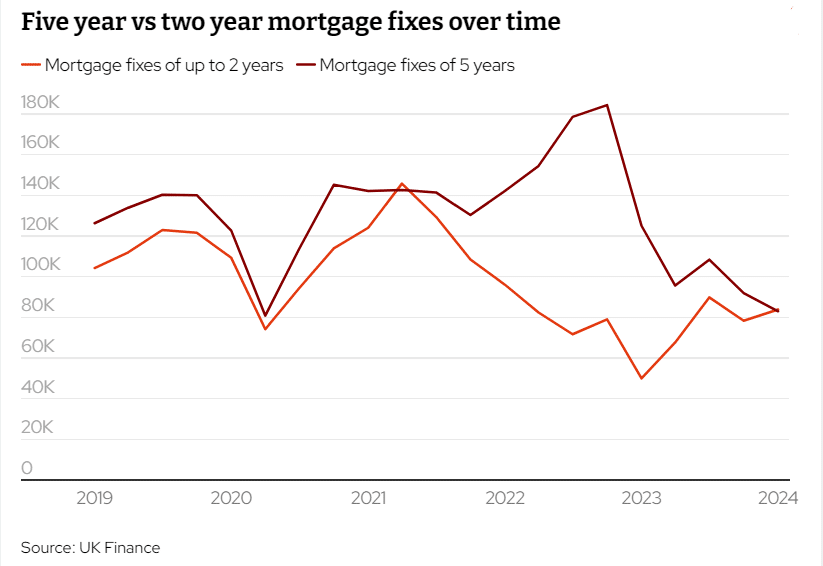

The Rise of Short-Term Mortgage Fixes

According to analysis of UK Finance figures from the beginning of 2019 to late 2023, the number of two year products being taken out was always lower than that of five-year loans, except one quarter. There were times when five year products being taken out were over twice as many as those being taken out on a two-year term.

In the first three months this year, there were 83,010 five-year fixes compared with 83,880 mortgages lasting less than two years. The previous year recorded only 125,060 five-year ones versus 50,020 less than two-year ones.

Lenders and brokers say that households are opting for shorter deals because they believe rates will go down within the next 2 years. This is so that, when their two-year fixes come to an end, they can then be able to move on to far cheaper deals instead of being locked in for five years.

MPowered Mortgages, however, said for those moving home 21 per cent of fixed-rate products selected were by a two-year period. In 2024 this percentage almost doubled to 38%.

“Demand for two-year fixed rates has doubled since the summer of 2022. Growth in demand for two-year fixes is in part due to people becoming more optimistic about the prospect of rates coming down in the future.” said Stuart Cheetham, CEO of MPowered Mortgages.

But he also stressed borrowers should be wary about where mortgage interest rates are going because no one knows what will happen to them. It is therefore worth speaking to a qualified financial adviser or broker before making any decisions.

“Many of our clients are taking two-year fixes rather than five-year deals, but this may change if five-year fixes continue to edge down and closer to 4 percent.” explained Aaron Strutt of Trinity Financial.

Understanding Fixed Rate Mortgages

Fixed rate mortgages typically follow swap rates, which reflect long-term predictions about the future direction of the Bank of England base rate. The base rate stands at today’s fifteen-year high at 5.25%, but there are suggestions it may fall later this year.

Based on the widely held view of economists, it is generally expected that the base rate will keep falling next year. Investors believe that this could come down to 4 percent in a year, but Capital Economics says this could fall to 3 percent, which would mean mortgage rates far below what’s currently available.

Two-Year Vs Five-Year Fixes

At present, five-year fixes are cheaper than two-year fixes. The average two-year fixed residential mortgage rate is 5.92%, while the average five-year mortgage rate today stands at 5.5% according to Moneyfacts.

However, customers who opt for a less expensive five-year deal might have no advantage if interest rates fall next year, hence forcing them to pay higher chargeable rates for five years.