Australia’s inflation has dipped slightly, offering a brief sense of relief. Yet this slowdown may prove misleading, as rising energy costs and global tensions begin to feed through the economy. Early signs suggest price pressures are far from contained, raising the prospect of a renewed surge in the months ahead.

A Fragile Slowdown in Consumer Prices

Latest figures from the Australian Bureau of Statistics (ABS) show annual inflation at 3.7% in February, down from 3.8% in January. The drop is small—almost easy to overlook—but it marks the first easing in a while. The trimmed mean, closely watched by the Reserve Bank of Australia (RBA), remains steady at 3.3%. That is still above the central bank’s target range of 2% to 3%.

At first glance, things seem to be settling. But February’s data doesn’t yet reflect the recent surge in oil prices. And that gap matters more than it might seem.

Energy and Food Costs Still Weighing on Households

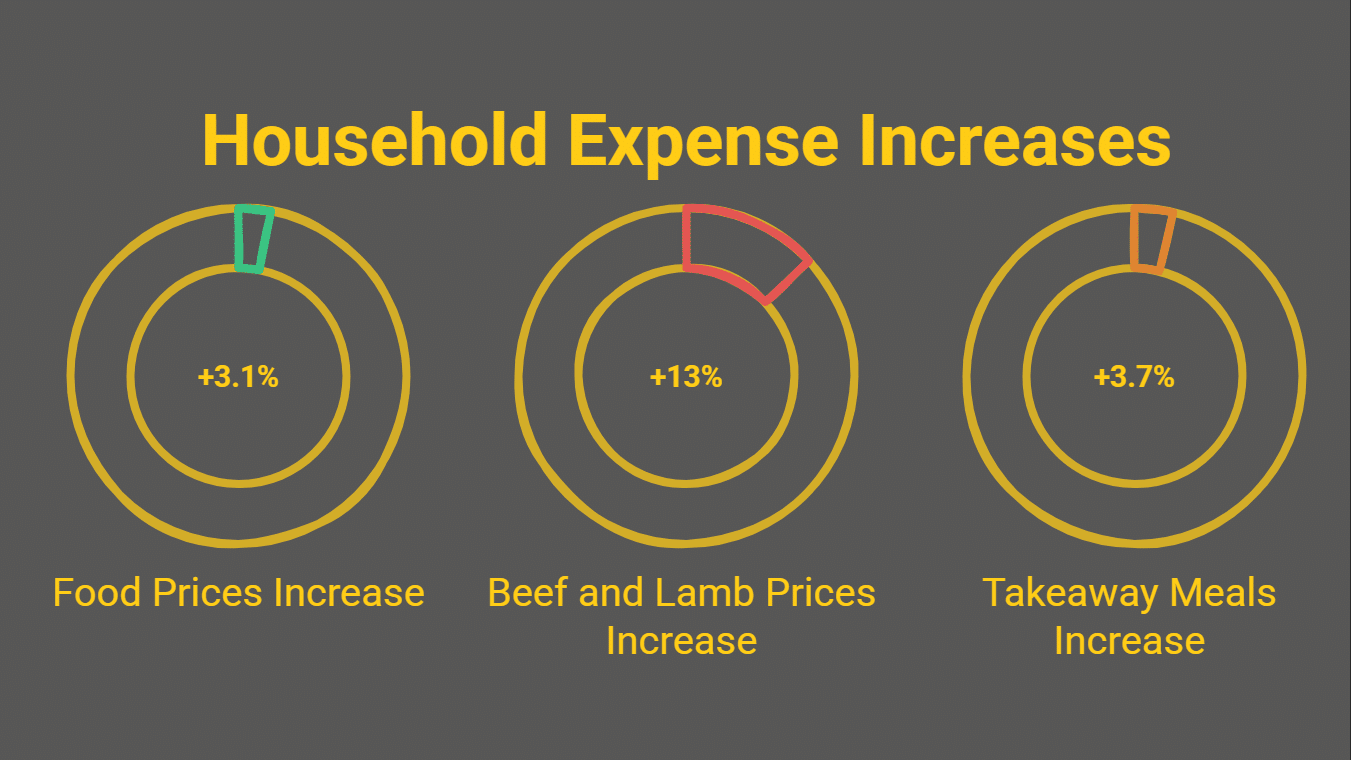

Over the past year, housing costs have been the main driver of inflation, largely due to energy. Electricity and gas prices have jumped by 37%, following the end of government rebates. For many households, that shift has been abrupt. Food prices have risen more moderately (+3.1%), but some items stand out. Beef and lamb prices are up 13%, while takeaway meals have increased by 3.7%. These are everyday expenses, so the pressure is felt quickly.

Interestingly, fuel prices were still 7.2% lower year-on-year in February. But that snapshot is already outdated. In recent weeks, petrol and diesel prices have surged past $3 per litre in some areas. The turnaround has been sharp—almost sudden.

Growing Pressure on Interest Rates

In this context, the RBA may continue tightening monetary policy. According to Canstar, a third consecutive rate hike could come as early as May. For borrowers, the effect is immediate. Monthly repayments could rise by around 7.4%, adding to an already stretched cost of living. It’s not just mortgages either—everything seems to be nudging higher at once.

RBA Governor Michele Bullock has signaled that further increases remain on the table if inflation does not slow enough. She has even acknowledged the possibility of an economic downturn. Not a certainty, but clearly a risk.

Forecasts Point to Inflation Climbing Again

Treasury scenarios are becoming less reassuring. If oil prices reach $120 per barrel, inflation could climb to 5.5%. Even a milder scenario, around $100 per barrel, would push inflation close to 5%. Major banks are broadly aligned with this outlook. Westpac expects inflation to hit 5.5% by mid-year, while Commonwealth Bank sees it moving above 5% if global tensions escalate further.

There is one nuance: underlying inflation, which excludes volatile items like fuel, is expected to rise more slowly—around 3.5%. Still, for households, it’s the visible prices that shape day-to-day reality.

An Outlook Shaped by Global Uncertainty

Two factors stand out: how long the Middle East conflict lasts, and how quickly the global economy stabilizes afterward. Both remain unclear, and that uncertainty feeds directly into inflation expectations. The Australian government has even drawn comparisons with shocks like the 2007 financial crisis or the COVID-19 period. It may sound dramatic, but it reflects a growing sense of vulnerability.

In the end, February’s slight dip looks more like a pause than a turning point. And pauses, in this kind of environment, rarely last long.