The most popular assumption about the new state pension is that you need to have contributed to National Insurance for 35 years to receive a full pension. However, this is a misconception. In reality, some of those who have contributed for more than 35 years are not entitled to a full pension, whereas others who have contributed for less time may receive the full amount.

The Calculation of the New State Pension

The calculation of an individual’s pension entitlement occurs in two main stages.

Step 1: Establishing the Foundation Amount

The first step is determining what is known as the “foundation amount.” This figure represents the greater of two calculations: the amount accrued under the old pension rules and the amount that would be calculated under the new rules.

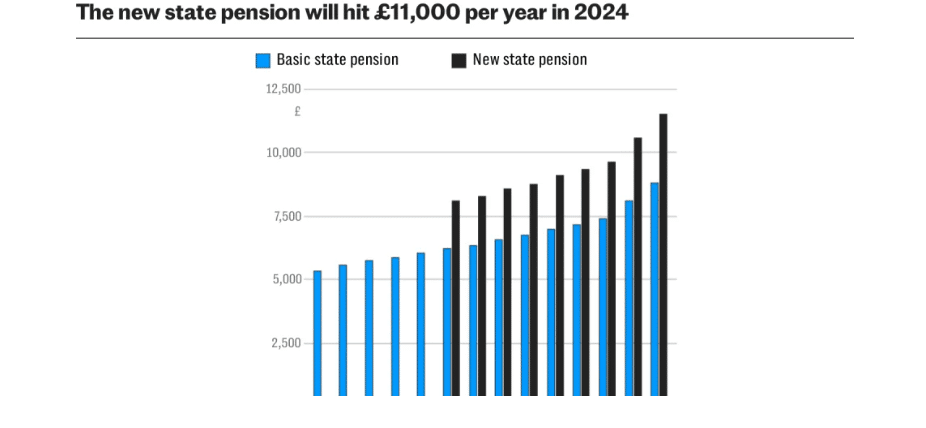

- Old Rules Calculation: This is based on a full basic pension, currently set at £156.20 per week, for those with 30 years or more of contributions. It also includes any additional earnings-related pension accrued, commonly known as SERPS or the State Second Pension.

- New Rules Calculation: This involves a full flat rate pension, currently £203.85 per week, for 35 years of contributions, but with significant deductions for any time spent “contracted out” into a workplace pension.

For individuals whose foundation amount exceeds the full flat rate, their pension is set at that amount but will still increase with inflation. Additional contributions made after the 2016-17 tax year will not affect this total.

Step 2: Contributions from 2016 to 2017 Onwards

From the financial year 2016–17 onwards, for each full year of contributions, an additional 1/35th of the full flat rate is added to the foundation amount. Therefore, with a full flat rate of £203.85, each year of additional contributions adds approximately £5.82 per week.

This structure allows those who have contracted out to gradually rebuild their entitlement to a full state pension, provided they make sufficient contributions after the specified date.

The Rationale Behind the Pension System Design

The two-stage process of determining the new state pension may appear unnecessarily complex. One might wonder why the government did not simply offer a full pension for 35 years of contributions, with a pro rata amount for fewer years. The answer lies in the concept of contracting out.

The Contracting Out Arrangement

Introduced in 1978 with the state earnings-related pension scheme (SERPS), the contracting out arrangement provided a mechanism for workers with existing employer pension schemes to opt out of SERPS. This arrangement allowed employers and employees to pay reduced National Insurance contributions, with the understanding that the workplace pension would offer benefits at least as good as those from SERPS.

When the government transitioned to a new single-tier state pension in 2016, it faced a dilemma regarding how to handle individuals who had spent years contributing at a lower rate.

Two extreme options were considered:

- To disregard past contracting out entirely, thereby granting a full pension to anyone with 35 years of contributions, regardless of their contribution rate.

- To permanently account for past contracting out, which would lead to ongoing deductions from the state pension for those who had contracted out.

The latter option would have resulted in many individuals remaining short of the new flat rate for decades, undermining the simplicity the new system sought to achieve.

To strike a balance, a compromise was reached: previous contracting out would be acknowledged through a one-time deduction in 2016, which could subsequently be offset by additional contributions made after this date.